Eversheds Sutherland | Michaela Walker, Michaela Arter, Julia Neal, Sumitra Subramanian and Thomas E. Pritchard

United Kingdom

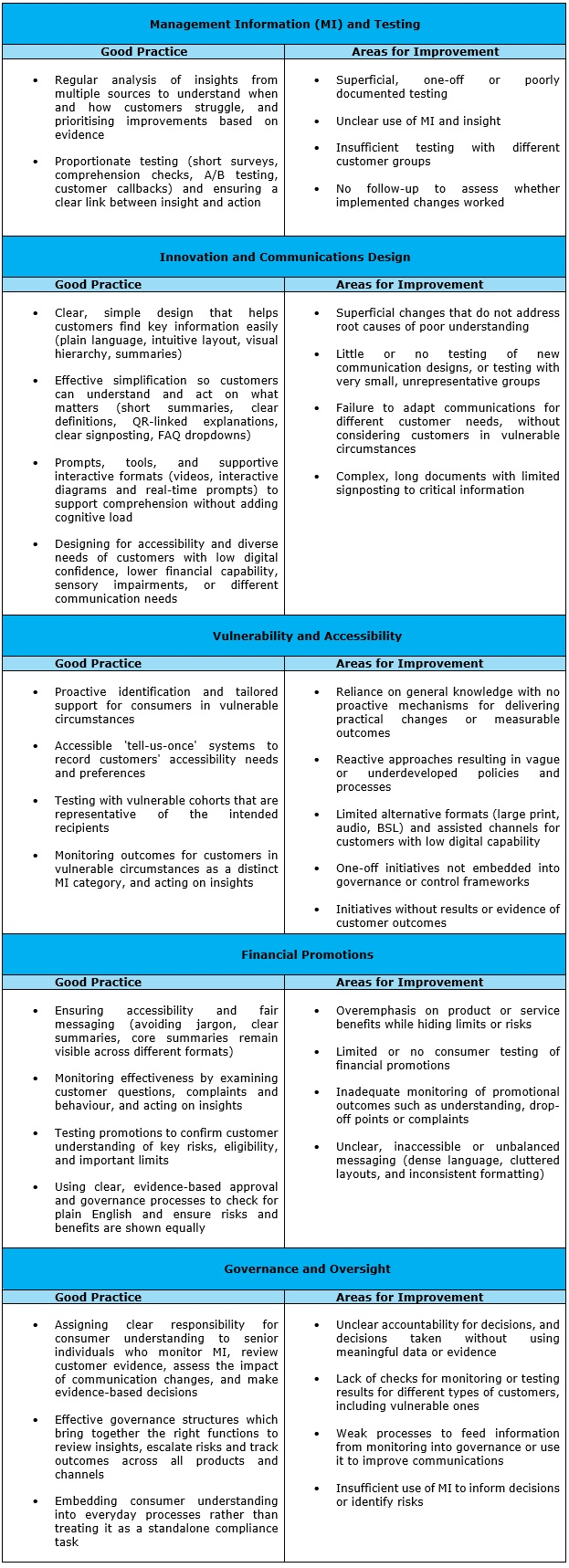

The FCA sets out the findings of its review into the consumer understanding objective of the Consumer Duty, highlighting good practice and areas for improvement.

Why should I read this?

The FCA’s report “Consumer understanding: good practice and areas for improvement” sets out its findings on how firms are delivering the consumer understanding outcome of the Consumer Duty (the Duty).

The consumer understanding outcome requires that the information firms give to customers must be:

- fair, clear and not misleading;

- presented at the right time; and

- presented in a way customers can understand.

The report highlights the FCA’s expectations of how firms should present information to customers and better support effective decision‑making.

What do firms need to know?

The examples of good and poor practice in the report do not create new regulatory requirements, and the FCA stresses that firms do not need to adopt every example. The FCA does, however, expect firms to use the examples to assess their own approaches and identify where they need to make improvements to ensure they are meeting their obligations under the Duty.

While the expectations apply to all firms that provide products or services to retail customers, firms may meet those expectations in a way that is proportionate to their scale and resources.

The report emphasises that to support consumer understanding, firms should ensure that their communication design, testing, monitoring, and governance form a coherent, end-to-end process.

How is the FCA enforcing the Consumer Duty?

Earlier this year, the FCA published its first Enforcement Watch newsletter which, alongside recent commentary from Therese Chambers, the FCA’s Co-Executive Director of Enforcement and Market Oversight, give a better idea of the FCA’s approach to enforcing the Consumer Duty.

Having initially given firms “time to breathe” as they embedded the Duty, the FCA has now started to take action, opening six investigations into suspected breaches, particularly in relation to fair value. All of the investigations are described as “edge” cases, where the firms under investigation appear to be outliers in terms of compliance with the Duty.

In relation to the consumer investment and asset management sectors, the FCA is also investigating firms on suspicions of misleading consumers and third parties with false statements. Such conduct could amount to a breach of the consumer understanding outcome as well as a breach of the fair, clear and not misleading rule under COBS 4.2.1(1)R.

The message to firms and senior managers is clear: if you fail to meet the FCA’s expectations relating to consumer understanding or the Consumer Duty more generally, you risk regulatory intervention including, where serious misconduct is suspected, investigation and enforcement action. This means it is critical to pay close attention to what the FCA says about compliance with the Duty and take action where you are falling short.

This article first appeared on Lexology | Source